Video: Global IoT market forecast (in billions of connected IoT devices)

Connected IoT device market update—Summer 2024

Number of connected IoT devices to grow 13% by end of 2024. According to IoT Analytics’ 171-page State of IoT Summer 2024 report, there were 16.6 billion connected IoT devices by the end of 2023 (a growth of 15% over 2022). IoT Analytics expects this to grow 13% to 18.8 billion by the end of 2024. This forecast is lower than in 2023 due to continued cautious enterprise spending as inflation and interest rates remain high—though are moderating—alongside continued chipset supply constraints and ongoing geopolitical conflicts in Eastern Europe and the Middle East. Despite the above macro factors, 51% of enterprise IoT adopters plan to increase their IoT budget in 2024 (with 22% of companies expecting a 10%+ budget increase compared to 2023).

This article is based on insights from:

State of IoT Summer 2024

Download a sample to learn about the in-depth data that are part of the report.

Download report sample

Already a subscriber? Browse your reports here →

Key executive quote on the IoT market outlook

“We expect [Qualcomm’s] IoT revenues to grow sequentially by low to mid-single digit percentage as we continue to see a gradual recovery from the macro factors impacting the industry.”

Akash Palkhiwala, CFO and COO of Qualcomm, May 1, 2024

Methodology

IoT Analytics counts connected IoT devices as active nodes/devices or gateways that concentrate the end-sensors, not every end node (sensor/actuator).

The following are communication technologies considered part of these connected IoT devices by time:

Wired– ethernet and field buses (e.g., connected industrial PLCs or I/O modules)

Cellular– 2G, 3G, 4G, and 5G

Low-power wide-area network (LPWAN)– Unlicensed and licensed low-power networks

Wireless personal area network (WPAN)– Bluetooth, Zigbee, Z-Wave, and the like

Wireless local access network (WLAN)– Wi-Fi and related protocols

Wireless neighborhood area network (WNAN)– Non-short-range mesh, such as Wi-SUN

Other– satellite and unclassified proprietary networks with any range

Computers, laptops, fixed phones, cell phones, and consumer tablets are not counted, and simple one-directional communications technology (e.g., RFID or NFC) is not considered.

IoT connections via more than one communication standard are only counted once.

Connected IoT devices forecast 2024–2030

Image: Global IoT market forecast (in billions of connected IoT devices)

40 billion IoT devices by 2030. The number of connected IoT devices is estimated to grow to 40 billion by 2030. Compared to its last IoT device market update in 2023, IoT Analytics slightly lowered its forecast for the number of IoT device connections after considering new market insights and recent market developments.

The lowered forecast is largely due to 3 reasons:

1. Economic concerns weigh heavily on investment confidence

Recent economic uncertainty likely to be felt for years. Throughout 2023 and into 2024, economic concerns remained the top topic of CEOs during earnings calls. Even if economic uncertainty fades throughout 2024, its impact on connected devices may be felt for years. End users and business confidence may take time to recover, leading to a wait-and-see approach to spending.

2. Chipset supply to remain a constraint for years to come in the face of surging demand

Chipset supply improves, but lead times remain high. Chipset supply has considerably improved in 2023 and 1H 2024, as demand has weakened in the face of a slowing economy. Despite the demand slump, current chip lead times remain elevated compared to pre-COVID-19 levels. While it is true that a lot of chip manufacturing capacity is being planned—fueled by government initiatives such as the US Chip and Science Act (2022) and the EU Chips Act (2022), it may take many years until supply matches or surpasses demand for the majority of different types of chipsets.

For example, Taiwan-based semiconductor company TSMC plans to initiate the construction of its fab in Dresden, Germany, by August 2024, and if there is no delay, the factory will be ready by 2027.

3. Chinese economic recovery taking time

A sluggish Chinese economy weighs heavily on IoT expenditures. China experienced muted economic growth in 2023, and deflationary pressures continue to exist, though they appear to be easing. The effects of this subdued growth are affecting Chinese industrial companies. At the end of June 2024, approximately 30% of Chinese industrial firms were losing money, beating the previous record set during the Asian financial crisis in 1998. Until the financial situation improves for these companies, new investments in industrial IoT are limited.

Global module inventory strategies lead to Chinese chipmaker closures. China has experienced renewed demand for cellular IoT modules (driven largely by public projects), which has helped deplete domestic module oversupply. However, much of the world is still employing low-inventory strategies to avoid or ease overstocking, and US sanctions on the import of Chinese-made chips continue. These strategies and sanctions limit the export of new IoT modules and chipsets, and just in 2023, nearly 11,000 Chinese chip and module-related companies ceased operations due to this.

Leading IoT connectivity technologies in 2023: 3 technologies make up nearly 80% of all IoT connections

Global IoT connectivity is dominated by three key technologies: Wi-Fi, Bluetooth, and cellular IoT:

1. Wi-Fi

Wi-Fi makes up 31% of all IoT connections. In 2023, 3/4th of Wi-Fi-enabled devices shipped worldwide were based on the latest Wi-Fi 6 and Wi-Fi 6E technologies, which promise faster and more reliable wireless connectivity than its predecessor, Wi-Fi 5. The adoption of these technologies has made communication between IoT devices more efficient, leading to improved user experiences and overall performance. Wi-Fi technology is leading IoT connectivity in sectors such as smart homes, buildings, and healthcare. Further, Wi-Fi 7 started to ship in 2024 and is expected to contribute to 7% of IoT-based Wi-Fi shipments.

2. Bluetooth

25% of connected IoT devices worldwide rely on Bluetooth. Bluetooth Low Energy (BLE), also known as Bluetooth Smart, has been continuously developed to allow IoT devices to maintain reliable connectivity while consuming limited power. As a result, BLE is now the preferred option for battery-powered IoT devices such as smart home sensors and asset tracking devices. Even the industrial sector is starting to show increasing interest in IO-Link Wireless technology, which is based on IEEE 802.15.1 (the technical standard for Bluetooth) and allows for wireless communication between sensors/actuators and an I/O master.

3. Cellular IoT

Cellular IoT (2G, 3G, 4G, 5G, LTE-M, and NB-IoT) now makes up nearly 21% of global IoT connections. According to IoT Analytics’ Global Cellular IoT Connectivity Tracker & Forecast (updated June 2024), global cellular IoT connections grew 24% YoY in 2023, strongly surpassing the growth rate for global IoT connections. This growth is due to the adoption of newer technologies such as LTE-M, NB-IoT, LTE-Cat 1, and LTE Cat 1 bis, as older technologies such as 2G and 3G are phased out.

Furthermore, 2024 marked the introduction of 5G RedCap technology. Unlike time-critical applications demanding stringent latency, RedCap-enabled IoT devices prioritize affordability and reduced complexity. With download speeds up to 150 Mbps, upload speeds of 50 Mbps, and latency under 100 ms, RedCap is propelling growth in consumer, enterprise, and industrial IoT devices. Notably, its suitability for high-quality video transmission is driving its adoption in video surveillance, offering a cost-effective alternative to standard 5G.

Wired IoT in 2023: 0.7 billion aggregation node connections vs. 23 billion end node connections

Video: Number of wired IoT connections 2023

There were 0.7 billion wired IoT aggregation nodes in 2023 but many more end nodes. Of the 16.6 billion IoT connections in 2023, 0.7 billion were wired IoT aggregation nodes—i.e., primary standalone devices that serve as central data transmission points, such as gateways, PLCs, IPCs, I/O-primaries, and routers—equaling 4% of the total IoT connections (see the main graph of this article). The remaining 15.9 billion connections were wireless IoT aggregation nodes and wireless IoT end nodes (i.e., wireless IoT devices with sensor capabilities relying on aggregation nodes for internet connectivity).

However, the number of wired IoT aggregation nodes only tells part of the story about global wired IoT connections. When going beyond just wired IoT aggregation nodes and looking at the wired IoT connection market in its totality—i.e., including wired IoT end nodes—IoT Analytics’ research found 23.4 billion wired IoT end nodes globally in 2023 (Note: the lead chart of this article does not consider wired IoT end nodes).

Wired IoT end nodes defined

IoT Analytics defines wired end nodes as devices with sensor capabilities that rely on other devices, such as aggregation nodes (e.g., gateway, PLC, IPC, I/O-Master, or router) for internet connectivity via a wired network connection.

The average aggregation node has 33 wired IoT end nodes. The ratio of wired IoT end nodes to aggregation nodes is projected to increase from 33 in 2023 to over 40 by 2030, fueled by both industrial and consumer IoT growth. Common examples of wired IoT end nodes include industrial field instruments, security cameras, smoke detectors, wired point-of-sale systems, and medical equipment. In a factory setting, this ratio can surpass 1:100; in other settings, e.g., in homes, it is often much lower.

Other State of IoT Summer 2024 research highlights

The report highlights a number of current developments in the IoT market. Here are 3 developments discussed in more depth in the report.

1. AI, including generative AI, AI + IoT, and edge AI

1. AI is at the forefront of corporate executives’ minds. The integration of AI in IoT, including generative AI (GenAI) and edge AI, is one of the key trends in 2024. CEOs discussed AI more than any other technology topic in earnings calls since Q1 2023, reaching 34% of calls in Q2 2024. The GenAI market went from nearly nothing to a hot market within a year.

2. Gen AI is entering the manufacturing domain. One of the key examples of this was the launch of Siemens Industrial Copilot.

3. Heavy investments into edge AI. Edge AI has emerged as a key theme in 2024. Edge AI is pivotal in enhancing safety, accuracy, and efficiency in IoT applications. US-based semiconductor manufacturers NVIDIA and AMD stand out as companies that play a crucial role in driving the adoption and implementation of edge AI technologies across various sectors.

“We stand on the brink of an era where edge AI will reshape our world in a profound way.”

Salil Raje, SVP of adaptive and embedded computing at AMD

2. Security

1. IoT malware attacks are on the rise. According to a 2023 ThreatLabz report, there was 400% growth in IoT-targeted cyber attacks over 2022. Manufacturing has been the sector most targeted for IoT attacks, with 54.4% of reported attacks.

2. Governments establish IoT security standards. To address the growing threat of cyber attacks against the rising number of IoT devices, country and regional governments are enacting legislation and programs aimed at stricter security. Earlier this year, the UK became the first country to mandate IoT cybersecurity standards, and the EU requires products sold in the EU to meet minimum standards. Additionally, the US has established a voluntary labeling program for wireless consumer IoT products.

3. Two cybersecurity approaches coming up. Two technology approaches, post-quantum cryptography (PQC) and zero trust security, also help address IoT security. PQC addresses the potential risk that the rise of AI presents—the ability to intelligently and quickly crack security algorithms. Zero Trust represents a security paradigm shift, whereby the security architecture focuses on securing every access request as though it originates from an open network, emphasizing the verification of every user and device. The strategy includes strong authentication mechanisms, micro-segmentation of networks, and continuous monitoring to detect and respond to threats.

Note: IoT Analytics went more in-depth about cellular IoT module security in a September 2023 article.

“AI will make it so much easier to crack weak implementations of algorithms that there will be no other choice than to use secure elements or secure MCUs to run cryptographic algorithms and to use strong software implementations of these algorithms.”

Ellen Boehm, EVP of IoT strategy and operations at Keyfactor

3. Sustainability

1. Sustainability is a key driver for IoT initiatives. While reviewing the top IoT stories in 2023, IoT Analytics noted that sustainability and ESG were the most accelerated drivers for IoT initiatives that year. Driving this acceleration then and now are climate and sustainability laws enacted by country and regional governments, such as the UK’s Sustainability Disclosure Standards, India’s Green Credit Rules, and the EU’s Renewable Energy Directive, to name a few. These laws appear to be affecting corporate thinking: between Q2 2019 and Q2 2024, boardroom discussions about sustainability rose from 9.4% of earnings calls to 23.6%.

2. IoT plays a key role in streamlined, automated sustainability reporting. With these and forthcoming corporate sustainability regulations coming into effect throughout the world soon, Companies are increasingly looking at sustainability data management solutions and IoT to streamline and automate their sustainability data management and reporting needs. IoT-based sensors, such as energy meters, water quality sensors, and air pollution monitors, are important technological building blocks for automating reporting. For example, energy meters can track and report real-time electricity usage, helping companies monitor and optimize their energy consumption, while water quality sensors measure parameters like pH, temperature, and turbidity, ensuring that water usage and disposal meet environmental standards.

“Combating climate change is the biggest task of our age. People are therefore right to expect companies to provide technical solutions to these issues.”

Stefan Hartung, CEO of Bosch

Disclosure

Companies mentioned in this article—along with their products—are used as examples to showcase market developments. No company paid or received preferential treatment in this article, and it is at the discretion of the analyst to select which examples are used. IoT Analytics makes efforts to vary the companies and products mentioned to help shine attention to the numerous IoT and related technology market players.

It is worth noting that IoT Analytics may have commercial relationships with some companies mentioned in its articles, as some companies license IoT Analytics market research. However, for confidentiality, IoT Analytics cannot disclose individual relationships. Please contact compliance(at)iot-analytics.com for any questions or concerns on this front.

Note: This article was updated in September 2024 to include the latest market data and insights from IoT Analytics.

Click to read previous analyses

State of IoT 2023: Number of connected IoT devices growing 16% to 16.7 billion globally

Article written by Satyajit Sinha on May 24, 2023.

IoT connections market update—May 2023

The latest IoT Analytics “State of IoT—Spring 2023” report shows that the number of global IoT connections grew by 18% in 2022 to 14.3 billion active IoT endpoints. In 2023, IoT Analytics expects the global number of connected IoT devices to grow another 16%, to 16.7 billion active endpoints. While 2023 growth is forecasted to be slightly lower than it was in 2022, IoT device connections are expected to continue to grow for many years to come.

IoT connections forecast

According to our analysis, by 2027, there will likely be more than 29 billion IoT connections. Compared to our last IoT device market update a year ago, we lowered our five-year IoT market outlook for two important reasons:

1. Chipset supply to remain constraint for years to come in the face of surging demand

Chipset supply chains have considerably improved in 2023 as demand has weakened in the face of a slowing economy. Despite the demand slump, current chip lead times remain elevated compared to pre-COVID-19 levels. We believe that once the economy recovers and a new demand wave kicks in, chipset supply will become much more constraint again. While it is true that a lot of chip manufacturing capacity is being planned as we speak,fueled by government initiatives such as the US Chip and Science Act (2022) and the EU Chips Act (2022), it may take many years until supply matches or surpasses demand for the majority of different types of chipsets.

Make no mistake, the investments into new chip manufacturing capacity are enormous. TSMC has increased its capital expenditure from approximately $15 billion in 2019 to $42–$44 billion in 2022. Similarly, in 2023, Samsung announced that it plans to invest $230 billion in South Korea over the next 20 years to build new chip production capacity. However, these investments take time to materialize. Semiconductor plant constructions typically take three to four years to complete, and it can take another three to four years for facilities to reach full capacity.

2. China uncertainties

In the last years, China was the leading country for new IoT device connections, with active cellular IoT connections in China alone surpassing two billion in 2022. However, the high growth years may be coming to an end with the country facing a number of issues, including technological supply shortages on the back of renewed US–China trade tensions, most notably in the semiconductor industry. In October 2022, the US placed an export ban on China, causing significant disruption to these industries. Consequently, chip companies are relocating their facilities outside of China. Some companies, such as Infineon, TSMC, AMAT, and ASML, have announced that they are moving parts of their production out of China.

The leading IoT connectivity technologies: three technologies making up nearly 80% of the market

Global IoT connectivity is dominated by three key technologies: Wi-Fi, Bluetooth, and cellular IoT.

Wi-Fi. Wi-Fi makes up 31% of all IoT connections. In 2022, more than half of Wi-Fi-enabled devices shipped worldwide were based on the latest Wi-Fi 6 and Wi-Fi 6E technologies, which promise faster and more reliable wireless connectivity. The adoption of these technologies has made communication between IoT devices more efficient, leading to improved user experiences and overall performance. Wi-Fi technology is leading IoT connectivity in sectors such as smart homes, buildings, and healthcare.

Bluetooth. 27% of global IoT connections rely on Bluetooth. Bluetooth Low Energy (BLE), also known as Bluetooth Smart, has been continuously developed to allow IoT devices to maintain reliable connectivity while consuming limited power. As a result, BLE is now the preferred option for battery-powered IoT devices such as smart home sensors and asset tracking devices. Even the industrial sector is starting to show increasing interest in IO-Link Wireless technology, which is based on IEEE 802.15.1 (the technical standard for Bluetooth) and allows for wireless communication between sensors/actuators and an I/O master.

Cellular IoT. Cellular IoT (2G, 3G, 4G, 5G, LTE-M, and NB-IoT) now makes up nearly 20% of global IoT connections.According to the Global Cellular IoT Connectivity Tracker & Forecast (Q1/2023 Update) by IoT Analytics, global cellular IoT connections grew 27% YoY in 2022, strongly surpassing the growth rate for global IoT connections. This growth is due to the adoption of newer technologies such as LTE-M, NB-IoT, LTE-Cat 1, and LTE Cat 1 bis, as older technologies such as 2G and 3G are phased out. Although 5G module shipments also grew more than 100% YoY in 2022, the growth rate is still slower than many had expected. In 2023, the top five network operators—China Mobile, China Telecom, China Unicom, Vodafone, and AT&T—managed 84% of all global cellular IoT connections. In terms of IoT revenue, the top five network operators make up 64% of the IoT network operator market, with China Mobile, AT&T, Deutsche Telekom (including T-Mobile), China Unicom, and Verizon leading the market.

Global cellular IoT market share – top 5 network operators

The analysis shows a few notable shifts over the years, for example:

China Mobile jumped from fifth place in 2012 to first place in 2021 and is expected to remain there in the foreseeable future.

AT&T, Verizon, and Deutsche Telekom have consistently ranked in the top five from 2010 to 2022 and are expected to maintain their positions through 2027.

China Unicom joined the top five in 2022 and is projected to remain among the leading network operators through 2027.

IoT connectivity trends to look out for

While the general IoT connectivity landscape only changes slowly (e.g., some devices remain connected for a decade or even longer), new IoT connectivity technologies do have an impact on the landscape in the long run. Here are two interesting developments we are monitoring (for more also visit our Embedded World conference 2023 takeaways and our MWC 2023 takeaways):

1. LPWAN technology convergence

In 2022, the LPWAN industry saw two significant events that shifted the focus from competition among LPWAN connectivity technologies to co-existence and convergence of those technologies. UnaBiz‘s acquisition of Sigfox and Semtech’s acquisition of Sierra Wireless paved the way for LPWAN companies to provide multi-connectivity of several LPWAN technologies at the same time. To make this convergence happen and be able to deploy any LPWAN technology, UnaBiz, for example, now collaborates with The Things Industries, Actility, Soracom, LORIOT, and others. This means that UnaBiz has become more than just a technology provider but rather a solution provider that also bundles all different technologies and orchestrates them on their own software platform. UnaBiz is just one example that shows how the industry is shifting from a single LPWAN technology view to a multi-connectivity solution view.

We anticipate that this LPWAN convergence may lead to the emergence of new multi-LPWAN connectivity modules in the future that would provide end-to-end connectivity in verticals such as logistics and mobility.

2. LEO-based satellite IoT connectivity

LEO satellite connectivity for IoT is gaining popularity because it provides extensive coverage, minimal delays, and strong reliability. The technology is especially useful in the agriculture, maritime, and logistics industries. LEO satellites are closer to Earth than traditional satellites, resulting in reduced latency and faster data transmission, which are essential for real-time data processing. This type of connectivity is more resilient and reliable, ensuring consistent communication, even in challenging environments or during natural disasters. Advancements in LEO-based IoT satellite connectivity continue to optimize performance and enhance the user experience.

According to IoT Analytics, satellite IoT connections are expected to grow from six million to 22 million between 2022 to 2027, at a CAGR of 25%. While this growth is expected to have a minor effect on the overall market, the integration of satellite connectivity options into LPWA chipsets by companies like Qualcomm could accelerate adoption. Sony Semiconductor already launched ALT1350, the first cellular IoT LPWA chipset to offer satellite connectivity, which opens up new possibilities for IoT devices to communicate beyond traditional network boundaries. This integration of satellite connectivity into LPWA chipsets is expected to drive further innovation and growth in the IoT market.

Other State of IoT (Spring 2023) research highlights

The 137-page report highlights a number of current developments in the IoT market. Here are three developments that are discussed in more depth in the report:

1. Predominantly positive IoT sentiment going into the second half of 2023

Despite a number of macro uncertainties and some (IoT-related) layoffs, the IoT market remains largely intact going into the second half of 2023. Most market participants have a predominantly positive outlook, with industrial IoT projects and Industry 4.0 initiatives driving the market. Below are some recent representative quotes from chip companies with a focus on IoT:

“We continue to secure major greenfield design wins, even amid macro uncertainty. The IoT market has incredible potential, with thousands of new applications on the horizon.”

Matt Johnson – President & CEO, Silicon Laboratories (1 February 2023)

“The industrial IoT markets are performing better than our expectations.”

Kurt Sievers – President & CEO, NXP Semiconductors (31 January 2023)

2. IoT platforms market is consolidating

Several major companies that were selling IoT platforms recently announced discontinuations, including Google’s IoT Core, Bosch‘s IoT Device Management, IBM’s Watson IoT Platform, and SAP’s IoT services. The reasons for the strategic shift away from IoT vary. The market dominance of Microsoft Azure IoT and AWS IoT in “generic” IoT platforms certainly played a role, in conjunction with the “the lack of profitability” in the offered IoT services. Several of these companies have announced a shift toward creating solutions specific to particular verticals or relying more on a few select partners to continue to support IoT initiatives (e.g., Google–Litmus Automation partnership).

“IoT services themselves don’t make enough money. The services like AWS IoT Core and Azure IoT Hub are expensive to build and maintain and by themselves they are likely not profit-making.”

Former IoT Product Lead, Microsoft

3. IoT-focused start-ups are struggling to secure funding

The amount of money invested in global IoT start-ups decreased significantly in the last 12 months. In the first quarter of 2023, we tracked 52 IoT-related funding rounds totalling $840 million, a 45% reduction in the value of investment in IoT start-ups companies compared to Q1/2022. Some of the larger recent IoT-related funding rounds include a $150 million Series D for US-based chipset manufacturer Astera Labs in November 2022 and a $43 million Series C for China-based connectivity chipset company XINYI Information Technology in March 2023.

Article written by Mohammad Hasan on May 18, 2022.

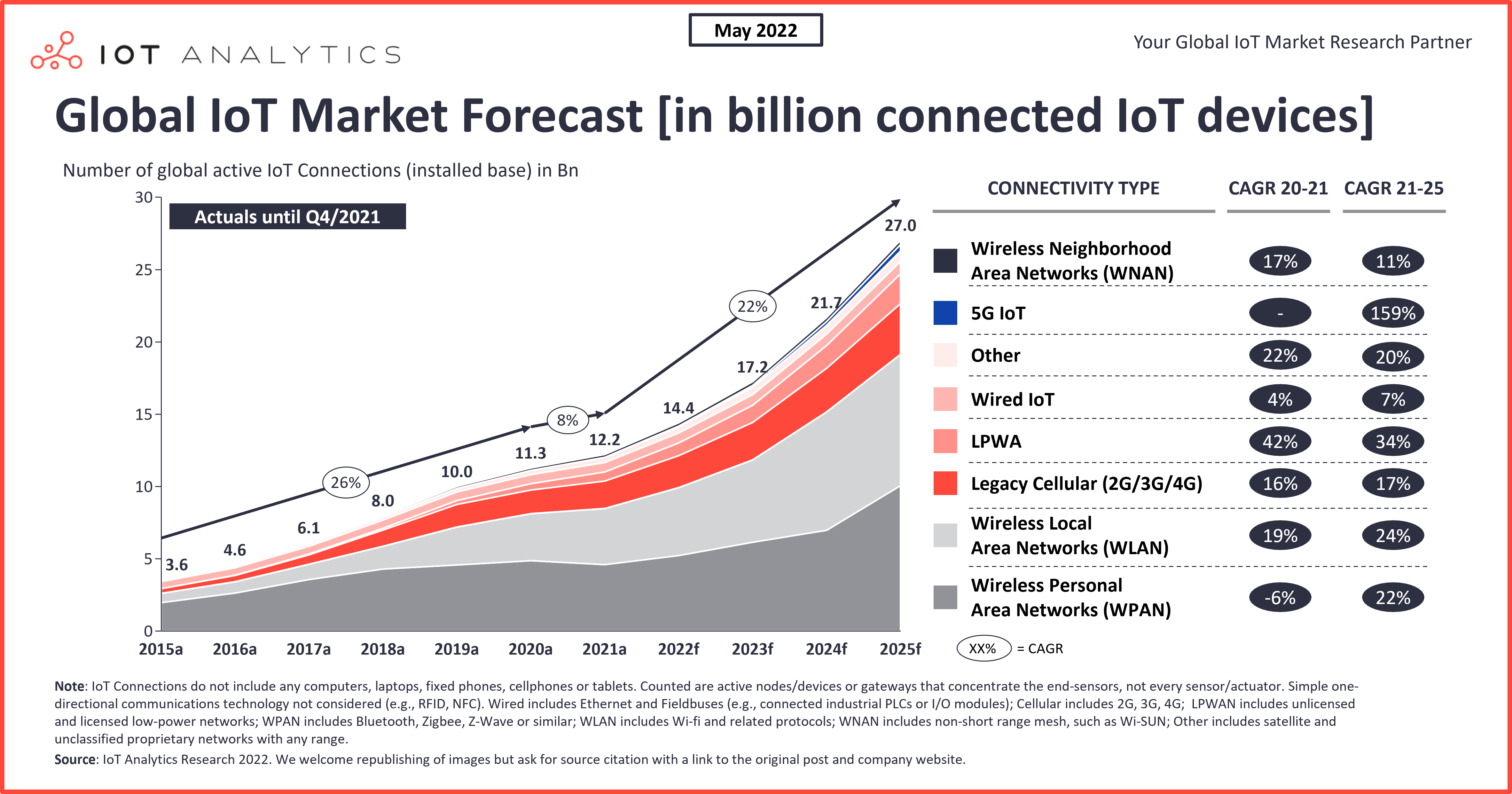

State of IoT 2022: Number of connected IoT devices growing 18% to 14.4 billion globally

IoT connections market update—May 2022

The chip shortage continues to slow the Internet of Things (IoT) market recovery, according to our latest State of IoT—Spring 2022 report, released in May 2022. The number of global IoT connections grew by 8% in 2021 to 12.2 billion active endpoints, representing significantly lower growth than in previous years.

Despite a booming demand for IoT solutions and positive sentiment in the IoT community as well as in most IoT end markets, IoT Analytics expects the chip shortage’s impact to the number of connected IoT devices to last well beyond 2023. Other headwinds for IoT markets include the ongoing COVID-19 pandemic and general supply chain disruptions. In 2022, the market for the Internet of Things is expected to grow 18% to 14.4 billion active connections. It is expected that by 2025, as supply constraints ease and growth further accelerates, there will be approximately 27 billion connected IoT devices.

Both the 2021 actuals and the current 2025 forecast for IoT devices are lower than previously estimated. (The previous estimate for 2021 was 12.3 billion connected IoT devices; the previous forecast for 2025 was 27.1 billion connected IoT devices).

Here is what impacted IoT connections in 2021, where we stand in 2022, and where we may be headed beyond 2022:

IoT in 2021: Selected IoT connection growth highlights

These are some key trends that impacted the growth of the number of connected IoT devices in 2021:

LPWA networks expanded, especially those using NB-IoT technology. NB-IoT adoption (finally) took off, with connections growing by 61% YoY, driven by a wide variety of implementations, most notably in the areas of water and gas metering.

Users are moving away from legacy 2G/3G toward 4G/5G IoT. 4G IoT connections grew by 24% due to higher adoption of LTE Cat 1-, Cat 4-, and Cat 6-based chipsets. For many implementations, LTE Cat 1 bis is becoming an alternative to the aforementioned LPWA technologies.

The chip shortage continued to slow the market recovery (see above).

COVID-19 continued to impact products and supply chains. In 2021, ongoing (local) COVID-19 restrictions resulted in many new and severe supply chain issues, such as a lack of vessels, trucks, and shipping containers and port congestion.

IoT in 2022: Current market sentiment

The current business sentiment for companies in digital and IoT remains predominantly positive although coming down from Q4 2021 highs. There is widespread acknowledgment that Covid-19 had an overall positive effect on the accelerated adoption of IoT technologies. This is confirmed by quotes from CEOs of IoT vendors and a sentiment analysis of earnings calls. The highest sentiments are found in companies offering connectivity services (sentiment score of 117), general software (115), cybersecurity (113), and cloud (113).

“Robust demand was again widespread across our end markets [in Q1 2022]. [] Overall, we continue to forecast favorable demand conditions to hold throughout the second half of this calendar year.“

Phil Gallagher, CEO at Avnet – April 27, 2022

“We are seeing continued momentum in key IoT markets, including industrial, enterprise, energy and first responder as more companies are collecting business-critical data from the edge of the network. The COVID-19 pandemic has accelerated Industry 4.0.”

Phil Brace, CEO at Sierra Wireless – May 12, 2022

From a regional point of view, sentiment in North America is leading (116), with APAC (103) lagging, specifically China, where fresh COVID-19 lockdowns are seen as a key threat to business growth in the region.

In our latest research, we highlight and discuss eight key macro themes to watch, many of which are interrelated. Here is a selection:

Inflation. Global growth forecasts are declining as inflation intensifies to >5% p.a. in most major economies of the world, raising expectations of increasing interest rates and a subsequent cooling down of the economy.

The ongoing war in Ukraine. The war in Ukraine is adding to supply disruptions and inflation concerns. The Minister of State for Electronics and Information Technology in India, Rajeev Chandrasekhar, for example, stated: “The Russia-Ukraine conflict has impacted supply chains in numerous sectors, including the semiconductor industry. The conflict may have particular impact on the supply of Neon and Hexafluorobutadiene gases, which are essential element[s] to manufacture semiconductor chips, as these are used in the lithography processes for chip production.”

The war for digital talent. Many companies are facing a massive challenge finding skilled labor to move ahead full force with digital transformation, AI, IoT, and cloud projects. IoT Analytics tracks online job ads on an ongoing basis. The number of job ads that included “IoT” grew by +32% between July 2021 and April 2022. Job ads including “AI” (+48%), “Edge Computing” (+53%), and “5G” (+52%) were in even higher demand.

As a result of some of these macro factors, particularly inflation, companies are forced to focus more on operational efficiency to neutralize cost pressures and ensure supply to customers.

Other State of IoT (Spring 2022) research highlights

Record levels of VC investments for IoT firms. Based on our research, Global VC funding for IoT-focused companies increased to a record of $1.2 billion in Q1 2022 compared to just $266 million in Q1 2021, with fewer deals in total but a number of very large funding rounds. Most recent investments centered around AI and analytics, cybersecurity, and IoT connectivity.

Several large IoT-focused acquisitions. IoT firms specializing in AI and analytics, IoT software, and semiconductors/chips collectively accounted for approximately 45% of all major IoT-related acquisitions between Q3 2021 and Q1 2022. Many of these deals were driven by the acquirer’s desire to create a more complete technology stack or product portfolio and reduce external dependency. Notable announcements include Panasonic’s acquisition of Blue Yonder ($8.5 billion) and Generac Power Systems’ acquisition of Ecobee ($770 million).

Summary

Growth in the number of connected devices slowed in 2021 but is expected to re-accelerate in 2022 and beyond. While new headwinds, such as inflation and prolonged supply disruptions, have emerged for the IoT market, the overall sentiment continues to be relatively positive, with the number of connected IoT devices expected to reach 14.4 billion by the end of 2022.

Article written by Satyajit Sinha on September 22, 2021.

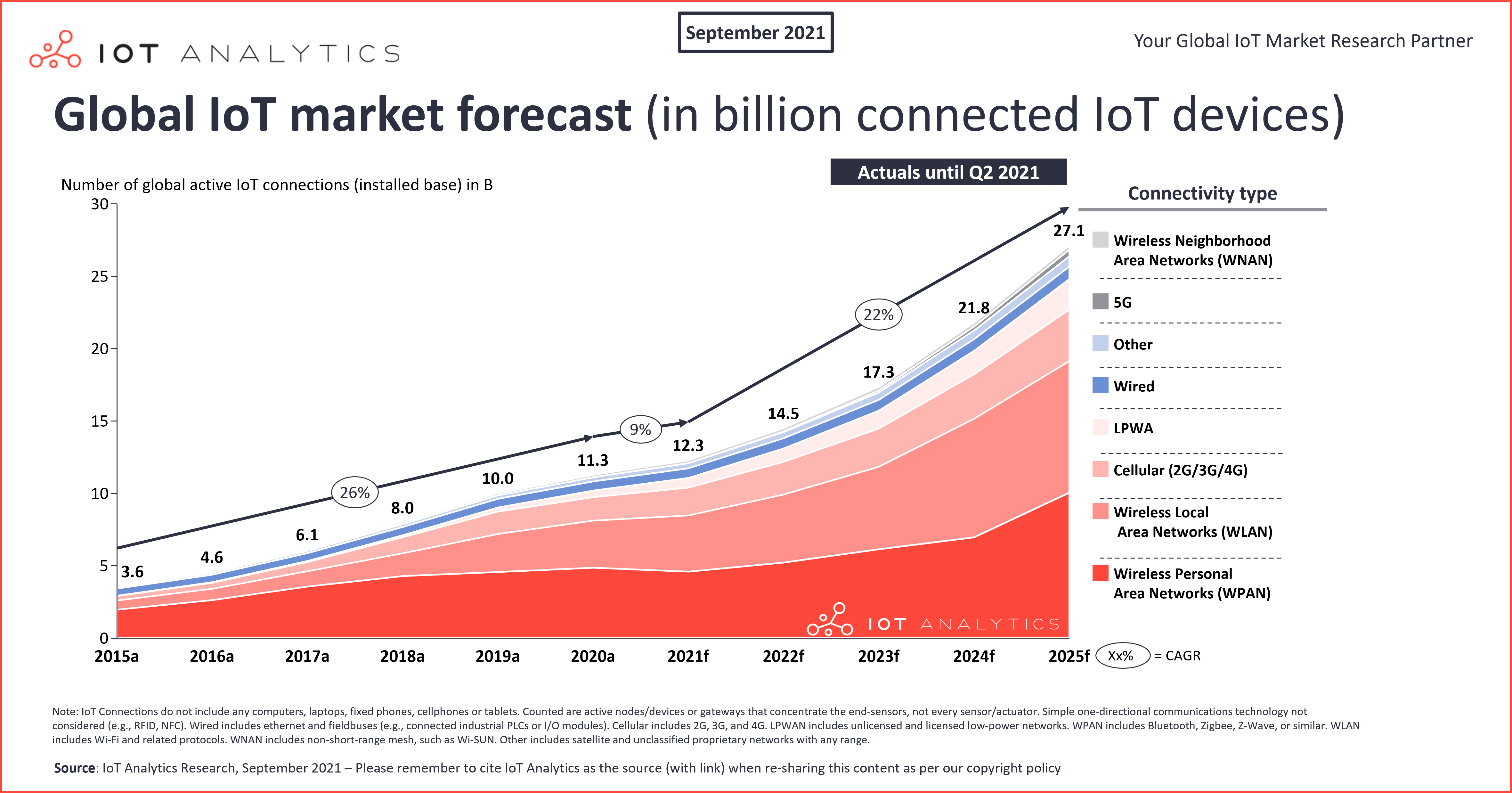

State of IoT 2021: Number of connected IoT devices growing 9% to 12.3 billion globally, cellular IoT now surpassing 2 billion

Market Update

Despite the chip shortage and COVID-19’s extended impact on the supply chain, the market for the Internet of Things continues to grow. In 2021, IoT Analytics expects the global number of connected IoT devices to grow 9%, to 12.3 billion active endpoints. By 2025, there will likely be more than 27 billion IoT connections.

This is one of many findings in IoT Analytics’ latest reports: State of IoT—Summer 2021 and the updated Cellular IoT & Low-Power Wide-Area (LPWA) Market Tracker (Q3 2021).

The 2020 actuals for the number of connected IoT devices came in slightly lower than the mid-year 2020 forecast (11.7 billion connected IoT devices forecasted for 2020 vs. actual of 11.3 billion). The forecast for the total number of connected IoT devices in 2025 has also been lowered to 27.1 billion (compared to 30.9 billion forecasted in 2020). Two critical factors are leading to the dent in the growth curve:

The COVID-19 pandemic: COVID-19 has impacted both demand and supply. Supply was reduced, as production was halted at times, and supply chains and access to raw materials were not intact. In the first half of 2020, budgets were frozen. In the second half of 2020, demand came back, but supply was often disrupted. Many IoT initiatives were halted or, in some cases, canceled in 2020. In 2021, COVID-19 effects have continued to significantly impact some regions, resulting in additional supply chain issues, such as a lack of vessels and shipping containers and port congestion.

The chip shortage: Initially, the chip shortage was a by-product of the COVID-19 impact on the supply chain. However, it has become its own issue; the supply capacity is not available to meet global chip demand. The chip shortage first impacted the automotive industry and then extended to other segments, such as smartphones, televisions, gaming, and IoT. In 2021, the chip shortage is expected to be a factor for up to two more years before enough additional production capacity becomes available. The current shortage is so pervasive that, of 3,000+ analyzed public companies, 11% mentioned “chip shortage” in their conference calls in the second quarter (Q2) of 2021.

These two factors are expected to have a negative impact for several years.

From a connectivity point of view, new technology standards, such as fifth-generation (5G), Wi-Fi 6, and LPWA, are driving device connections. A wildcard in the mix is satellite IoT, which could make a bigger impact toward the latter part of the forecast period.

It is important to note that, while the forecast for the total number of IoT connections has been lowered due to the aforementioned reasons, IoT markets, in general, are accelerating post-COVID-19 (as previously reported). The IoT acceleration is driven by investments into additional software tools and applications and the required integration. Global enterprise IoT spending in 2020 grew 12.1%, reaching $128.9 billion as reported earlier in the year.

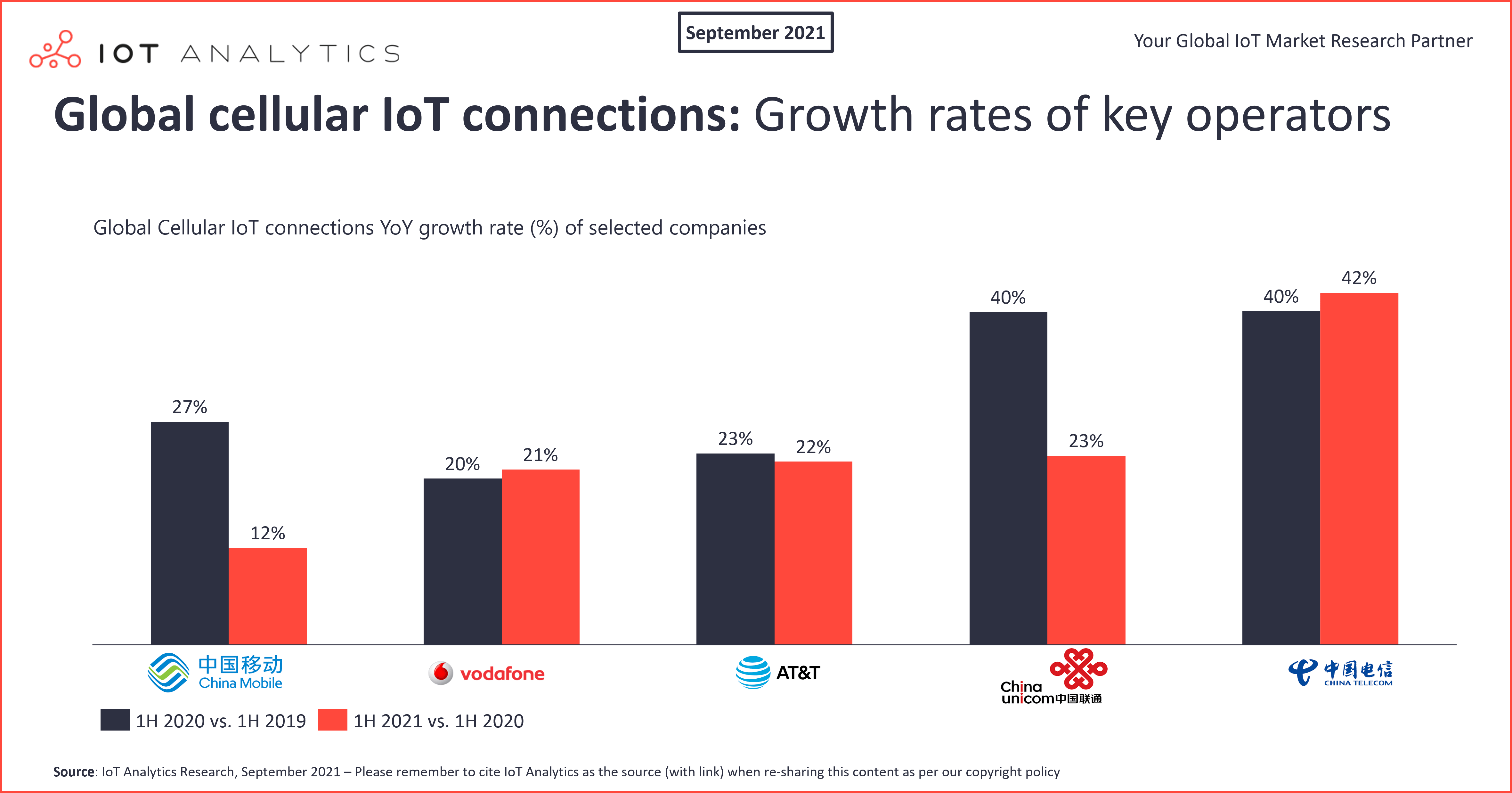

Cellular IoT market deep dive: two billion active connections by the end of Q2 2021

The number of connected IoT devices using cellular technology grew 18% year-over-year (YoY) to reach 2 billion by the end of the first half (1H) of 2021. China Mobile, China Telecom, and China Unicom account for almost three-quarters of the market. In the past 12 months, China Telecom grew 42% and increased its market share by more than two percentage points. Vodafone continues to lead the global market outside of China with a 6% global market share. US-based AT&T grew 22% YoY and held a 4% global market share in 1H 2021. IoT initiatives in China during the last 1.5 years were much less affected by COVID-19 and, in many cases, continued as planned after a short COVID-19 lockdown.

Regarding cellular technologies, the decline of 2G and 3G IoT connections continues, while the mass deployment of 5G connections is anticipated to start this year. Fourth-generation long-term evolution (4G LTE) connections grew 25% YoY due to higher adoption of the long-term evolution category 1 (LTE-Cat 1) and LTE-Cat 1 bis subsegments.

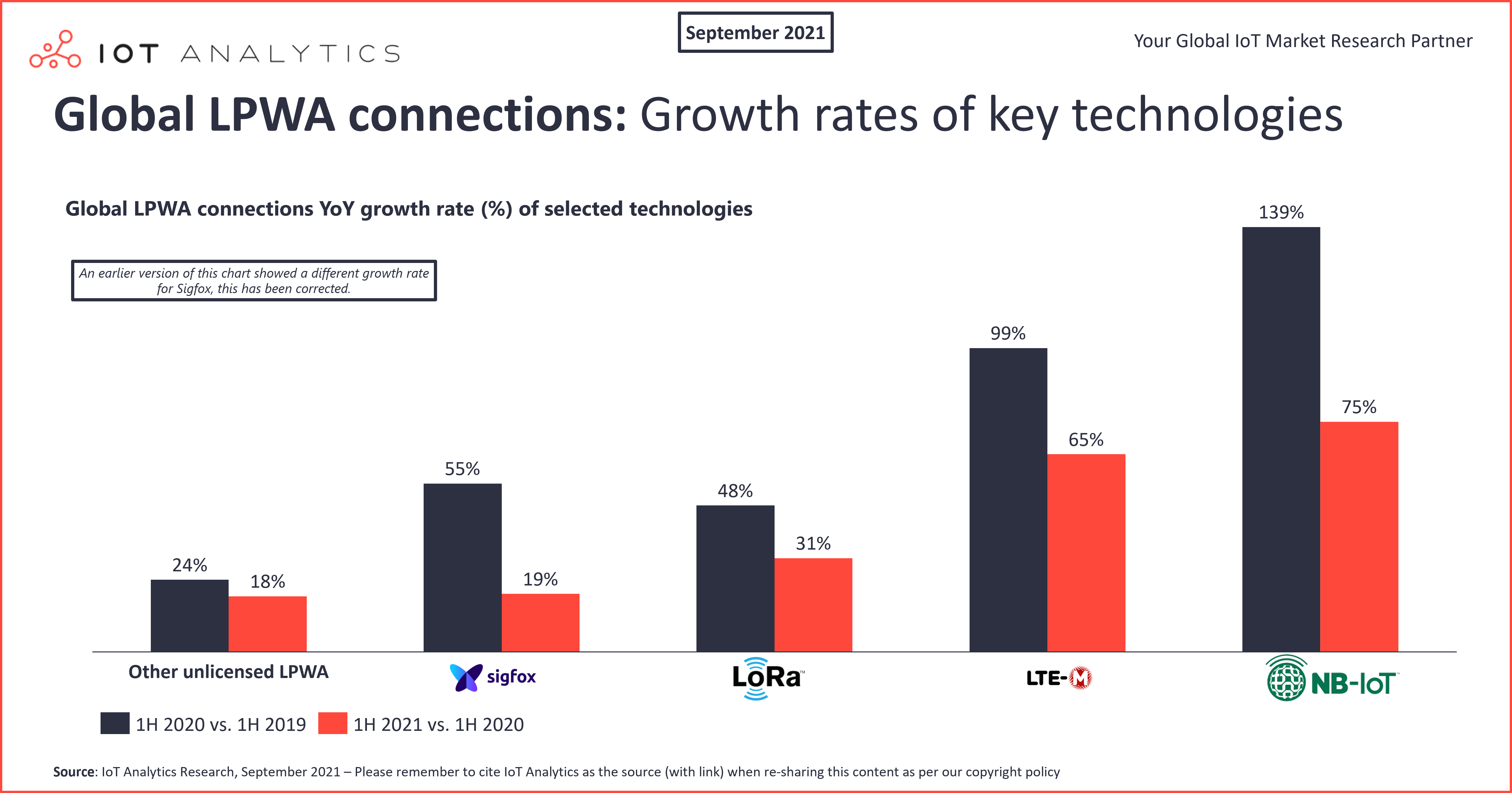

LPWA market deep dive: licensed LPWA market now larger than unlicensed LPWA

In 1H 2020, the share of connected IoT devices using unlicensed LPWA (e.g., long range (LoRa) and Sigfox) led with a 53% share, and licensed LPWA (i.e., narrow-band IoT (NB-IoT) and LTE-machine-type communication (LTE-M)) contributed 47% of global LPWA connections. A year later, licensed LPWA leads with a 54% share, while unlicensed LPWA has a 46% share of global LPWA connections. A key reason is that NB-IoT connections grew 75% YoY in 1H 2021. NB-IoT as a single technology now dominates the LPWA connection market with 44% market share, and LoRa has slipped to second place with a 37% share of global connections.

In the last 12 months, asset tracking and monitoring were the key applications driving unlicensed LPWA growth, while growth in NB-IoT was driven by smart meters and buildings and infrastructure industry verticals.

IoT Analytics expects that NB-IoT and LoRa/LoRaWAN will continue to dominate the market in the coming five years, with LTE-M and Sigfox in distant third and fourth places, respectively. While other technologies will continue to exist, at this point, it does not appear as though they will play a significant role in the overall global market, although they remain attractive for certain niche applications.

Look out for an updated 2021 low-power wide-area network (LPWAN) market report with plenty of detail on the LPWA market in Q4 2021.

End of previous analyses.

More information and further reading

Are you interested in learning more about the IoT market?

State of IoT Summer 2024

A comprehensive 171-page report on the current state of the Internet of Things, incl. market update, forecast, latest trends, and more.

Download report sample

Already a subscriber? See your reports here →

Related market data

You may be interested in the following IoT market data products:

Global IoT Enterprise Spending

Global Cellular IoT Connectivity Tracker & Forecast

Related publications

You may be interested in the following publications:

IoT Use Case Adoption Report 2024

IoT Startup Landscape and Database 2024

Industrial Connectivity Market Report 2024–2028

IoT Enterprise Projects Adoption Report 2024

Related articles

You may also be interested in the following recent articles:

IoT Startup Landscape 2024: 7 notable insights

Global cellular IoT connectivity market reached $15B in 2023, 5G set to drive further growth

IoT market update: Enterprise IoT market size reached $269 billion in 2023, with growth deceleration in 2024

Top 5 enterprise technology priorities: AI on the rise, but cybersecurity remains on top

Are you interested in continued IoT coverage and updates?

Subscribe to our newsletter and follow us on LinkedIn and Twitter to stay up-to-date on the latest trends shaping the IoT markets. For complete enterprise IoT coverage with access to all of IoT Analytics’ paid content & reports including dedicated analyst time check out the Enterprise subscription.

Leave a Comment